IWSR 2018 Global Beverage Alcohol Data Shows Growth in Spirits, but Beer and Wine Volume is Down; Market Expected to Grow by 3% Over Next 5 Years

Beverage alcohol drinkers across the globe consumed a total of 27.6bn nine-litre cases of alcohol in 2018, but while that number represents a decrease of -1.6% from the year prior, new data from the IWSR forecasts that total alcohol consumption will steadily increase over the next five years, to 28.5bn cases in 2023.

In terms of retail value, the global market for beverage alcohol in 2018 was just over $1tn, a number which the IWSR expects to grow 7% by 2023 as consumers continue to trade up to higher-quality products.

These figures – and more than 1.5m other points of data – are included in the just-released IWSR Drinks Market Analysis Global Database, which also shows:

Gin was the Leading Global Growth Category in 2018, and Forecasted to Reach 88m Cases by 2023

The largest gain in global beverage alcohol consumption in 2018 was in the gin category, which posted total growth of 8.3% versus 2017. Pink gin was a key growth driver, helping the category sell more than 72m nine-litre cases globally last year. In the UK alone, gin was up 32.5% in 2018, and the Philippines (the world’s largest gin market) posted growth of 8%, fueled by a booming cocktail scene and premiumisation

of the market. By 2023, the gin category is expected to reach 88.4m cases globally, with particular strong growth in key markets such as the UK, Philippines, South Africa, Brazil, Uganda, Germany, Australia, Italy, Canada and France. Notably, Brazil has emerged as a new hotspot for the category, with volumes there more than doubling last year and forecasted to grow at 27.5% CAGR 2018-2023, as the gin-and-tonic trend has increased in upmarket bars of São Paulo and Rio de Janeiro.

Consumption of Whisky and Agave-Based Spirits Continues to Increase

Spurred by innovation in whisky cocktails and highballs, the global whisky category increased by 7% last year, driven in large part by a strong Indian economy (whisky grew by 10.5% in India, as consumers continue to trade up in the category). The US and Japan posted 5% and 8% growth, respectively. The IWSR forecasts whisky to grow by 5.7% CAGR from 2018 to 2023, to almost 581m nine-litre cases. Also, continued interest in tequila and mezcal (especially in the US), and innovation in more premium variants and cocktails, drove the agave-based spirits category to 5.5% global growth in 2018 – and is expected to post 4% growth over the next five years (2018-2023 CAGR).

Mixed Drinks and Cider Grow

The mixed drinks category (which includes premixed cocktails, long drinks, and flavoured alcoholic beverages) grew 5% globally in 2018. By 2023, it is projected that more than 597m nine-litre cases of mixed drinks will be consumed across the world. The growth is backed by continued strong gains in ready-to-drink (RTD) cans in the US and Japan, the category’s two largest markets. In Japan, most RTDs are locally made and almost exclusive to Japan. Their popularity is partly due to the fact that

they are relatively dry, which makes them more food-friendly and sessionable. In the US, the popularity of alcohol seltzers has been a tremendous engine for growth in the RTD market. In the cider category, as investment levels in those products continue to rise, almost 270m cases are expected by 2023, a 2.0% CAGR 2018-2023. Both of those categories (mixed drinks and cider) are taking share from beer as perceived accessibility increases (less bitter, easier to drink.)

Vodka, Liqueurs, and Cane Spirits are in Decline

Vodka lost volume in 2018 (-2.6%) as the market for lower-priced brands continued its decline in Russia and the Ukraine (two of the largest markets for this spirit). Higher-priced vodkas, however, showed a more positive trend last year. Nonetheless, the outlook for total vodka over the next five years remains sluggish as the category is forecasted at -1.7% CAGR 2018-2023. Also in decline is the flavoured spirits category (liqueurs), which dropped by -1.5% globally in 2018, and is expected to continue to slip in 2019 before rebounding slightly in 2020. Cane spirits (primarily Brazilian cachaça) was down -1.6% last year, and is forecasted to lose another 4.5m cases by 2023.

Beer Continued to Lose Volume in 2018, but is Expected to Rebound

Global beer declined -2.2% in 2018, impacted greatly from volume decreases in China (-13%). Other large markets such as the US and Brazil also fell (-1.6% and -2.3%, respectively), while Mexico and Germany saw growth (6.6% and 1%, respectively). The future outlook for beer, however, paints a more positive picture, as the category is expected to show a slight increase in 2019 and post a 0.7% CAGR 2018-2023.

Wine Volume Declines, but Value Increases

Wine, which had posted strong global growth in 2017, lost -1.6% in volume in 2018 as wine consumption declined in major markets such as China, Italy, France, Germany and Spain (the US market was flat). However, though consumers are drinking less wine, they’re increasingly drinking better – pushing wine value to increase. Globally, the retail value of wine is projected at $224.5bn by 2023, up from $215.8bn in 2018. The one bright spot in wine volume is the sparkling wine category, which is expected to show a five-year CAGR of 1.17% 2018-2023, driven in large part by prosecco.

Low- and No-Alcohol Products on the Rise

Low- and no-alcohol brands are showing significant growth in key markets as consumers increasingly seek better-for-you products, and explore ways to reduce their alcohol intake. Growth of no-alcohol beer is expected at 8.8%, and low-alcohol beer at 2.8%. No-alcohol still wine is forecasted at 13.5%, and low-alcohol still wine at 5.6%. Growth of no-alcohol mixed drinks is predicted at 8.6%. (Above figures are all CAGR 2018-2023.)

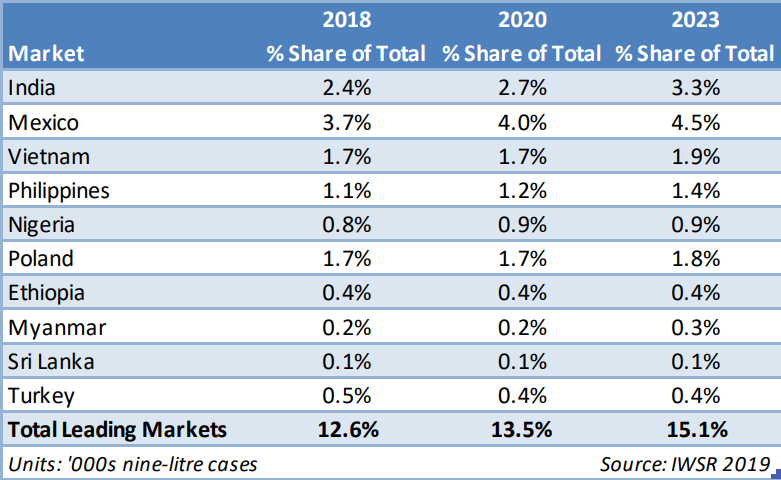

Top Ten Performing Global Markets, 2018-2023

A look at the world’s fastest-growing beverage alcohol markets shows an emergence across a variety of developing countries. A combination of growing legal-drinking-age populations and healthy economies is driving some of this growth, which is expected to continue over the next five years.

“Every year our analysts spend months traveling the world to speak with suppliers, wholesalers, retailers, and other beverage alcohol professionals to assess what is happening market by market in this fast-changing business,” says Mark Meek, the IWSR’s CEO. “The raw data we collect is enormously valuable, but equally important is what that data tells us in terms of trends, challenges, and opportunities facing the industry.”

Cheese and garlic naan bomb starter is a must try. Tiny naan discs served as starter with cheese and garlic stuffing had the right flavours.

Cheese and garlic naan bomb starter is a must try. Tiny naan discs served as starter with cheese and garlic stuffing had the right flavours.

With dishes inspired from the western coast, the menu not only includes the names of the dishes, but also the place they are inspired from. Signatures include Khakhra from Gujarat, Tadka Hummus from South India, Amritsari Fish from Mangalore and Prawns Koliwada from Mumbai, find your tastebuds, taking a ride along the coast too. The grill section, includes the basics like, Cheese Seekh, Achari Aloo, Fish Tikka and Masala Prawns. The nouveau main course section has dishes like, Truffle Oil and Okra Khichadi, Chicken Gassi, and Goan Fish Curry and Rice.

SHOR promises you endless stories and binging sessions over the course of its journey. With a menu that is carefully hand-picked and curated which is juxtaposed with music, this place is sure to win your heart.

With dishes inspired from the western coast, the menu not only includes the names of the dishes, but also the place they are inspired from. Signatures include Khakhra from Gujarat, Tadka Hummus from South India, Amritsari Fish from Mangalore and Prawns Koliwada from Mumbai, find your tastebuds, taking a ride along the coast too. The grill section, includes the basics like, Cheese Seekh, Achari Aloo, Fish Tikka and Masala Prawns. The nouveau main course section has dishes like, Truffle Oil and Okra Khichadi, Chicken Gassi, and Goan Fish Curry and Rice.

SHOR promises you endless stories and binging sessions over the course of its journey. With a menu that is carefully hand-picked and curated which is juxtaposed with music, this place is sure to win your heart.

sign that the Scotch Whisky industry remains confident about the future. This is great news for our many employees, our investors, supply chain and, of course, for our consumers all over the world, who love Scotch.

“This report also highlights the high rate of domestic tax that Scotch Whisky faces in the UK. In the US, Scotch and other whiskies are taxed at just 27% of the rate that HM Treasury taxes us here at home. We will continue to press the Chancellor for fairer treatment of Scotch Whisky in our domestic market, which reflects the vital economic contribution the thousands of people who work in whisky make to the UK economy every day.”

sign that the Scotch Whisky industry remains confident about the future. This is great news for our many employees, our investors, supply chain and, of course, for our consumers all over the world, who love Scotch.

“This report also highlights the high rate of domestic tax that Scotch Whisky faces in the UK. In the US, Scotch and other whiskies are taxed at just 27% of the rate that HM Treasury taxes us here at home. We will continue to press the Chancellor for fairer treatment of Scotch Whisky in our domestic market, which reflects the vital economic contribution the thousands of people who work in whisky make to the UK economy every day.”

contributes more than double than life sciences (£1.5bn) to the Scottish economy, supporting more than 42,000 jobs across the UK, including 10,500 people directly in Scotland, and 7,000 in rural communities.

contributes more than double than life sciences (£1.5bn) to the Scottish economy, supporting more than 42,000 jobs across the UK, including 10,500 people directly in Scotland, and 7,000 in rural communities.

A growing spirits distribution sector worldwide – especially in France where there were now between 20 and 30 national distributors compared with three or so 29 years ago – was further evidence of trade and consumer demand.

Trends pushing spirits expansion are: revivals of traditional spirits such as Calvados and Armagnac where there was growing interest in Asia; rediscovery of locally-produced spirits, eg Irish Whisky, Gin and Vodka; global interest in little-known spirits such as Mezcal; new exotic spirits such as agricultural rum from Tahiti, “where no spirits at all were made 10 years ago”.

A growing spirits distribution sector worldwide – especially in France where there were now between 20 and 30 national distributors compared with three or so 29 years ago – was further evidence of trade and consumer demand.

Trends pushing spirits expansion are: revivals of traditional spirits such as Calvados and Armagnac where there was growing interest in Asia; rediscovery of locally-produced spirits, eg Irish Whisky, Gin and Vodka; global interest in little-known spirits such as Mezcal; new exotic spirits such as agricultural rum from Tahiti, “where no spirits at all were made 10 years ago”.

“A stable government is indeed welcome for the nation and economy. We hope that the new government will reinforce its progressive policies towards the industry, and usher in the next phase of reforms to promote ease of doing business and ‘Making in India’. We also look towards the Federal government to encourage states to urgently bring comprehensive regulatory reform into key state- GDP contributing sectors such as alcoholic beverages,” says, Anand Kripalu, Managing Director and CEO, Diageo India.

“A stable government is indeed welcome for the nation and economy. We hope that the new government will reinforce its progressive policies towards the industry, and usher in the next phase of reforms to promote ease of doing business and ‘Making in India’. We also look towards the Federal government to encourage states to urgently bring comprehensive regulatory reform into key state- GDP contributing sectors such as alcoholic beverages,” says, Anand Kripalu, Managing Director and CEO, Diageo India. The beer industry has its fair share of challenges. And with the competition heating up and input prices rising it is becoming difficult to invest in growth. “With a strong mandate that the government has received, we look forward to sustained reforms that will spur further growth in the economy. We also look forward to continued emphasis on ease of doing business,” says Shekhar Ramamurthy, Managing Director, United Breweries Ltd.

The beer industry has its fair share of challenges. And with the competition heating up and input prices rising it is becoming difficult to invest in growth. “With a strong mandate that the government has received, we look forward to sustained reforms that will spur further growth in the economy. We also look forward to continued emphasis on ease of doing business,” says Shekhar Ramamurthy, Managing Director, United Breweries Ltd. “It is indeed a blessing that India has elected a strong and stable Goverment and I look forward to more structural reforms so that India can continue on a strong growth trajectory with gainful employment for all its citizens. I also expect the federal goverment to build consensus amongst all states to include potable alcohol in GST,” said Deepak Roy, ABD Vice Chairman.

“It is indeed a blessing that India has elected a strong and stable Goverment and I look forward to more structural reforms so that India can continue on a strong growth trajectory with gainful employment for all its citizens. I also expect the federal goverment to build consensus amongst all states to include potable alcohol in GST,” said Deepak Roy, ABD Vice Chairman. But now companies are scaling down their volumes where the margins are thinner, introducing premium brands and focussing on profits. Diageo is working to get consumers to ‘premiumise’. The company is working to taking a long term view and creating business value. The history associated with Diageo’s iconic brands, too, bears testimony to such far-sightedness.

But now companies are scaling down their volumes where the margins are thinner, introducing premium brands and focussing on profits. Diageo is working to get consumers to ‘premiumise’. The company is working to taking a long term view and creating business value. The history associated with Diageo’s iconic brands, too, bears testimony to such far-sightedness.

While congratulating on the grand come back of PM Narendra Modi, Dr. Lalit Khaitan, Chairman of Radico Khaitan Ltd. says, “The voters have endorsed Modi’s decisive leadership, his ability to take the country from red tape to red carpet, his government’s multiple schemes to pull out millions from abject poverty and provide them essential services like electricity, cooking gas, bank accounts and free health services.”

While congratulating on the grand come back of PM Narendra Modi, Dr. Lalit Khaitan, Chairman of Radico Khaitan Ltd. says, “The voters have endorsed Modi’s decisive leadership, his ability to take the country from red tape to red carpet, his government’s multiple schemes to pull out millions from abject poverty and provide them essential services like electricity, cooking gas, bank accounts and free health services.” KALS CMD Mr.S Vasudevan says on the historic victory of the NDA government, “I wish our Honourable Prime Minister Mr. Modi for his impeccable victory. This is a well-deserved victory for transforming our nation in terms of controls, governance, and GDP growth. I personally look forward to having reforms in the IMFL Industry as well that contributes significant revenue to the respective states. I wish the new government all the very best and I’m confident under the leadership of our Honourable PM, India will get into the strides of excellence.”

KALS CMD Mr.S Vasudevan says on the historic victory of the NDA government, “I wish our Honourable Prime Minister Mr. Modi for his impeccable victory. This is a well-deserved victory for transforming our nation in terms of controls, governance, and GDP growth. I personally look forward to having reforms in the IMFL Industry as well that contributes significant revenue to the respective states. I wish the new government all the very best and I’m confident under the leadership of our Honourable PM, India will get into the strides of excellence.” And having overcome the legacy issues associated with the USL acquisition, Diageo claims to have set itself the ambitious target of “changing the alcohol industry in India”. Much of that effort revolves around a campaign to inculcate the spirit of ‘responsible drinking’, which translates into reinforcing moderation, and in promoting road safety in collaboration with State governments.

And having overcome the legacy issues associated with the USL acquisition, Diageo claims to have set itself the ambitious target of “changing the alcohol industry in India”. Much of that effort revolves around a campaign to inculcate the spirit of ‘responsible drinking’, which translates into reinforcing moderation, and in promoting road safety in collaboration with State governments.

India is a country of diverse cultural heritage and as Indians, we love to savour this diversity indistinct with mouth-watering cuisines from all parts of the country.

India is a country of diverse cultural heritage and as Indians, we love to savour this diversity indistinct with mouth-watering cuisines from all parts of the country.

rural employment numbers. Today, almost 510 farmers from Maharashtra and Karnataka are working with Sula with assured buy back contracts.

rural employment numbers. Today, almost 510 farmers from Maharashtra and Karnataka are working with Sula with assured buy back contracts.

Beam Suntory in India has offices in Gurgaon, New Delhi, Mumbai, Bangalore, Hyderabad, Kolkata and a primary bottling facility in Rajasthan.

Beam Suntory in India has offices in Gurgaon, New Delhi, Mumbai, Bangalore, Hyderabad, Kolkata and a primary bottling facility in Rajasthan.